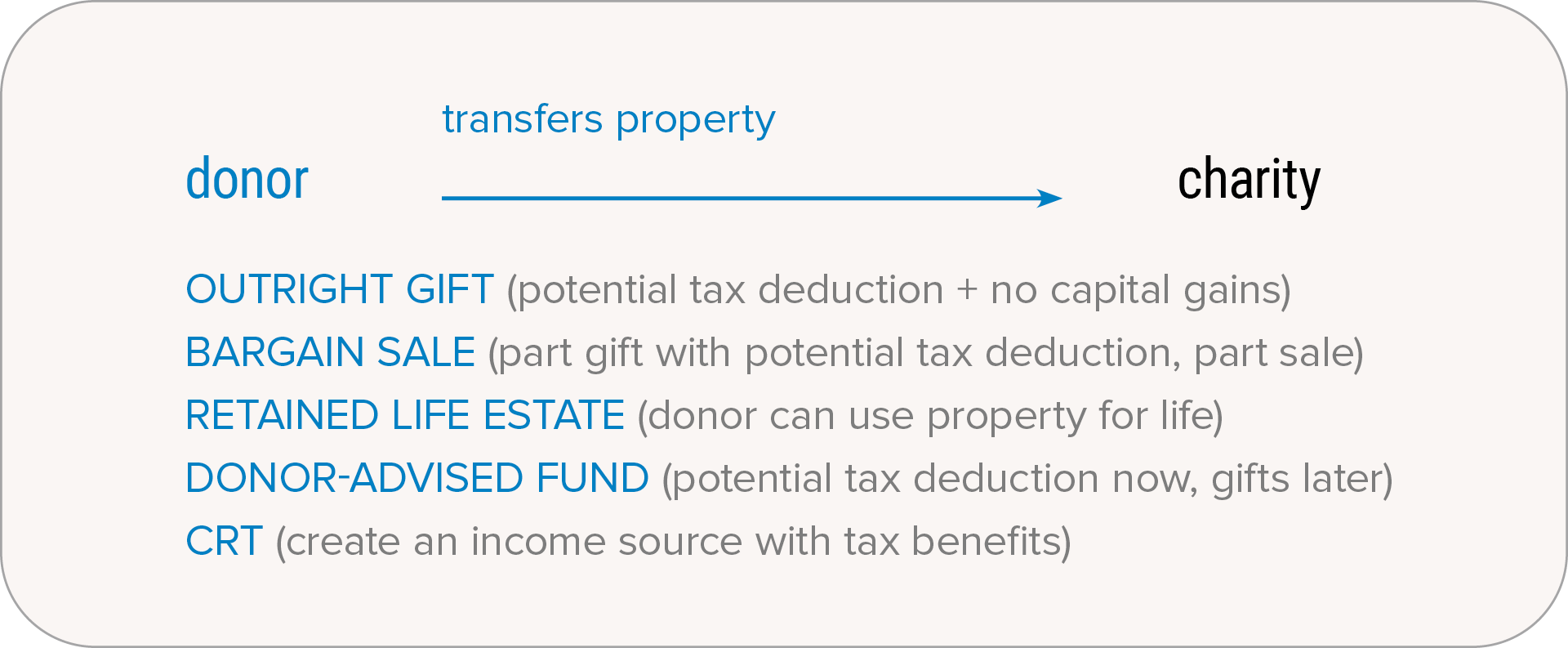

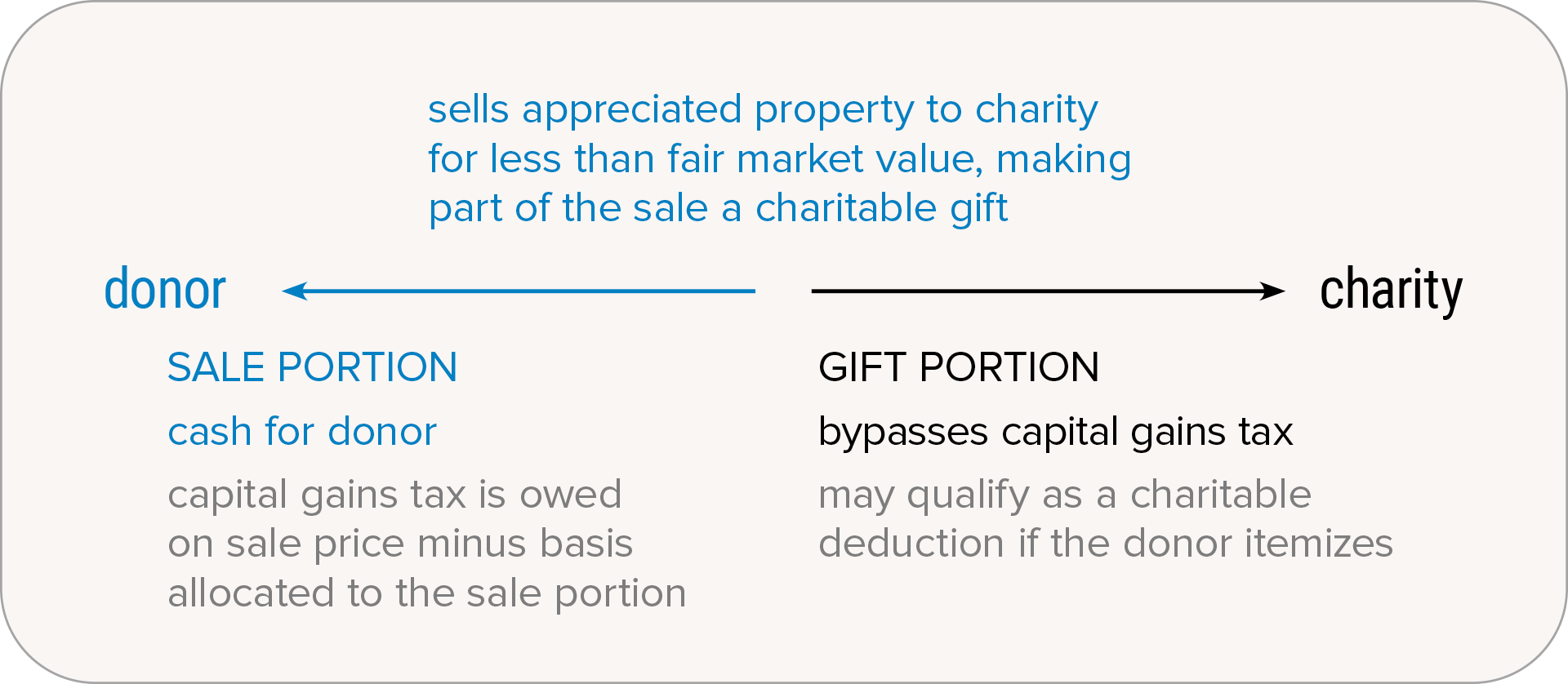

OPTION 2: A Bargain Sale

You may find this option useful if you are ready to dispose of your property but aren’t in a position to give it away. A bargain sale is part gift and part sale, and therefore, provides both a current income tax deduction and proceeds from the sale of the property. It works like this:

- You sell the property to the Foundation for less than its full fair market value—for example, if you sell us a property appraised at $500,000 for only $200,000.

- In the above scenario, you receive the $200,000 sale price, but you also make a $300,000 gift to us.

- The gift portion qualifies for an income tax charitable deduction (subject to limitations).

- No capital gains tax is due on the gift portion.

OPTION 3: A Gift of a Remainder Interest

You may find this is the perfect solution if you could use an income tax deduction now but would like to continue to use and/or occupy the personal residence or farm for the rest of your life. It works like this:

- You enter into an arrangement with the Foundation under which the property will be irrevocably transferred to us at the time of your death.

- You retain a “life estate” that gives you the right to live on or use the property throughout your lifetime.

- Even though the gift doesn’t actually take place until later, because it is irrevocable, your gift qualifies for an immediate income tax deduction for the discounted present value of our future interest in the property (essentially, the value of the land and improvements reduced by the value of your lifetime use of the property).

- After making a gift of a remainder interest, if you decide you no longer need the property, you can choose to donate your life estate and receive an additional charitable deduction at that point. (Note that there will be issues with this option if it appears to the IRS that you planned to do this all along.)

OPTION 4: A Gift to Establish a Charitable Remainder Trust

You may find this to be a helpful option if you want to get rid of your property and establish an income stream to supplement other forms of retirement income. It works like this:

- You give your property to establish a charitable remainder trust (CRT).

- The trustee (which could be Southwestern Medical Foundation) is able to sell the property without incurring any capital gains tax.

- The trustee can then invest the sale proceeds and use the money to make regular income payments to you and/or your named income beneficiaries for life or for a stated term of years.

- At the end of the trust term, the remaining trust assets will pass to Southwestern Medical Foundation.

Read more about charitable remainder trusts.

Evaluate the Fit

A gift of real estate may be a particularly good option to consider if you:

- Own appreciated property (residential, commercial, or undeveloped land) you no longer wish to use or maintain

- Would like to get rid of your property while reducing or even eliminating any capital gains tax on the appreciation

- Could use a charitable deduction

- Want to use your property to establish an income stream

- Are willing to put in a bit more time and effort to use this asset to meet both financial and charitable goals in a tax-efficient manner

See How it Works

Scott and Robin’s vacation cottage, once a family joy, has become a burden. They thought about selling the property and giving the proceeds to Southwestern Medical Foundation, but when they learned that we would accept the cottage as an outright gift, it was an ideal solution. Scott and Robin itemized in order to receive a tax deduction (with a qualified appraisal), eliminated the cost and hassle of a sale, and owed no capital gains tax on the property’s significant appreciation. We then sold the cottage and put the full amount of the proceeds to work supporting our health care mission—as a qualified charity, we did not owe any capital gains tax on the sale.